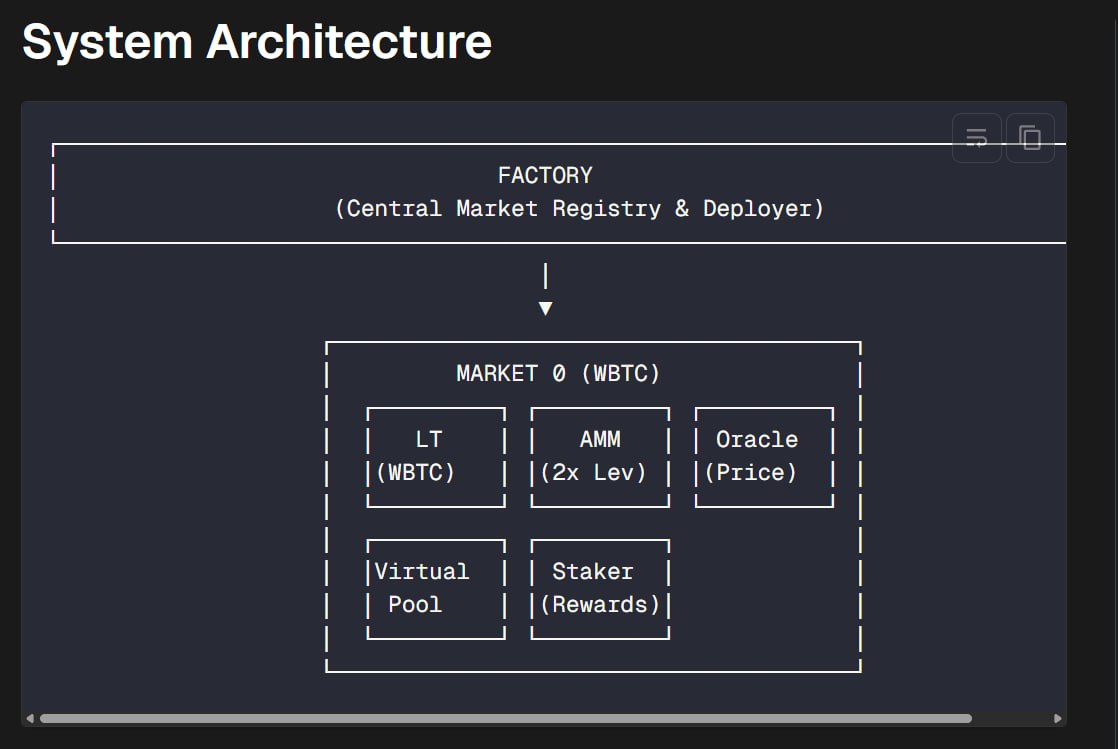

Yield Basis has published a technical overview detailing how its markets provide constant 2x leveraged exposure to Curve LP positions while aiming to eliminate impermanent loss for depositors. The documentation explains the protocol’s contract architecture, math, and market structure, giving developers and advanced users a clearer view of how the system maintains its target leverage and isolates risk across markets.

According to the new docs, each Yield Basis market is built around a Curve Cryptoswap LP position (initially BTC and ETH-related pools) and gives users 2x compounding leverage on that LP exposure via an automated market maker (AMM) that continuously rebalances positions. BTC (or other supported assets) is paired with borrowed crvUSD in a dedicated CDP, the resulting Curve LP token is used as collateral, and a bonding-curve-based AMM manages the relationship between collateral and debt to keep an effective 2x leverage ratio. The overview includes the key equation used by the AMM and defines parameters such as the leverage-squared constant (LEV_RATIO) that allow the system to algorithmically maintain the target leverage.

The release matters because Yield Basis is positioning itself as a new class of AMM that offers BTC and other asset holders spot-like exposure without impermanent loss, while still generating fee-based yield. By publishing detailed technical documentation, the project is giving auditors, integrators, and sophisticated DeFi users the information needed to evaluate protocol design, understand how markets remain isolated (e.g., separate instances for cbBTC, WBTC, tBTC, ETH), and assess the risks of its leveraged, crvUSD-backed structure. This transparency is particularly relevant given Yield Basis’s rapid TVL growth, the existence of its YB governance/utility token, and its role in experiments around sustainable, non-subsidized on-chain yield for blue-chip assets.

✨ AI-generated background, compiled from web sources — not editorial content.